| | In this article we use an example from November 2012 to help explain an interesting relationship between the cost of gold lease rates and the spot gold price, and how this might be used for trading gold online. When the lease rates for gold are reduced sharply over a 2 or 3 day period the price of gold tends to also drops quickly – what’s really interesting is that the gold sell-off takes place a day or two after the reduction in the lease rates and therefore it is possible to use these sharp lease rate reductions as forward indicators of price action. |

We have to make clear we are not claiming to be the first to recognise this, nor is this a fool-proof method for forecasting price – there are many good articles detailing research into this freely available across the web and there are also many conspiracy theorists that see this as pure market manipulation by the big players. We are not one of the conspiracy theorists – we are just gold traders trying to use every available resource at our disposal to create the best chance possible for success.

After a number of failed attempts to break through $1734 throughout November, gold finally punched its way through on the 23rd, triggering many technical buys as traders foresaw prices rising back towards the $1785-$1795 level. It came as a surprise to most of us when the price stalled out around $1755 and then fell away sharply on the 27th back down to $1700 and, later, to $1683.

After a number of failed attempts to break through $1734 throughout November, gold finally punched its way through on the 23rd, triggering many technical buys as traders foresaw prices rising back towards the $1785-$1795 level. It came as a surprise to most of us when the price stalled out around $1755 and then fell away sharply on the 27th back down to $1700 and, later, to $1683.

The sell-off on the 27th was in fact so unexpected that the CME Group, which operates the U.S. COMEX gold futures market, had to issue a statement to confirm that there had not been a “fat-finger” data entry error that caused the market to slump.

So what caused the price to drop so suddenly?

Keeping things as simple as possible; the gold lease rate (GLR) is calculated as LIBOR (London Inter-Bank Offered Rate) minus GOFO (Gold Forward Offered Rate), with LIBOR being the average interest rate at which a selection of London banks will lend money to each other at and GOFO being the interest rate at which dealers will lend gold on swap against US dollars.

Central banks lease their gold to provide liquidity. The Central bank will lease their gold to a bullion bank at the agreed GLR for a set duration (1, 3, 6 or 12 months) – the bullion bank uses the gold to create a profit by selling the gold and using the money to invest in something which yields higher returns, using these returns to pay off the lease costs on the gold.

Since 2008, it is normal for the 1-month GLR to be negative and, quite often, the 3-month GLR falls below zero too. In effect, the Central bank is paying the bullion bank to take their gold – this might sound strange, but as the value of physical gold has shot up in recent years so has the cost of things like insurance and storage and so it makes sense for someone else to be bearing these costs whilst you effectively still retain the asset.

If, for whatever reason, the GLR is suddenly and dramatically cut a flood of selling (and therefore drop in the price of gold) takes place as the bullion banks take advantage of the lower leasing rates to “acquire” more gold to sell so as to raise more capital to invest in higher yield securities and thus increase their profits.

We’ll leave it to you to surmise the different reasons why these sharp drops in the GLR take place – as we said previously, we are not conspiracy theorists. What we do know is that, between 23rd November and 26th November 2012 the 1, 3, 6 & 12-month GLRs fell quite sharply and that this was followed on the 27th by an unexpected fall in the gold price from $1749 to a low of $1684 over the next 5 days. By the 27th the GLRs had returned to their pre-fall levels, but gold nose-dived $65 against the trend.

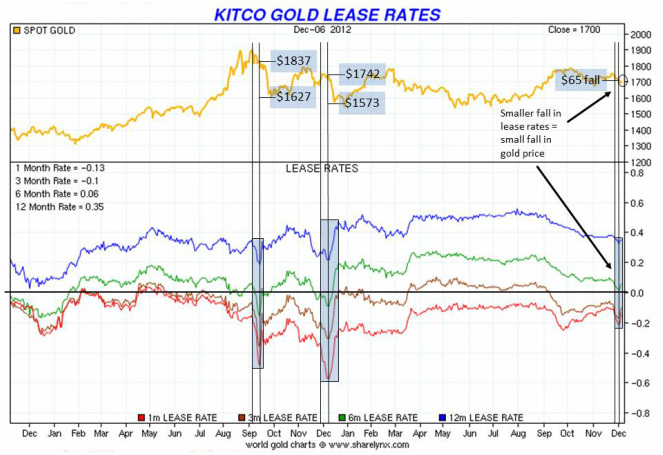

This can be seen with even greater clarity in September 2011 and December 2011 when you look at the chart below:

Central banks lease their gold to provide liquidity. The Central bank will lease their gold to a bullion bank at the agreed GLR for a set duration (1, 3, 6 or 12 months) – the bullion bank uses the gold to create a profit by selling the gold and using the money to invest in something which yields higher returns, using these returns to pay off the lease costs on the gold.

Since 2008, it is normal for the 1-month GLR to be negative and, quite often, the 3-month GLR falls below zero too. In effect, the Central bank is paying the bullion bank to take their gold – this might sound strange, but as the value of physical gold has shot up in recent years so has the cost of things like insurance and storage and so it makes sense for someone else to be bearing these costs whilst you effectively still retain the asset.

If, for whatever reason, the GLR is suddenly and dramatically cut a flood of selling (and therefore drop in the price of gold) takes place as the bullion banks take advantage of the lower leasing rates to “acquire” more gold to sell so as to raise more capital to invest in higher yield securities and thus increase their profits.

We’ll leave it to you to surmise the different reasons why these sharp drops in the GLR take place – as we said previously, we are not conspiracy theorists. What we do know is that, between 23rd November and 26th November 2012 the 1, 3, 6 & 12-month GLRs fell quite sharply and that this was followed on the 27th by an unexpected fall in the gold price from $1749 to a low of $1684 over the next 5 days. By the 27th the GLRs had returned to their pre-fall levels, but gold nose-dived $65 against the trend.

This can be seen with even greater clarity in September 2011 and December 2011 when you look at the chart below:

As you can see from the chart above, the cuts to the GLR which have a strong impact on price are typically followed with a more-or-less immediate return to their previous levels. It also seems that the larger and sharper the GLR cut is, the heavier and quicker the impact on the gold price – in the September and December examples above the subsequent gold price falls were $210 and $169 respectively…but in both cases you can see that the GLR cut took place, had reached its bottom and was on the turn prior to the sell-off.

Can we trade using this information?

Like with all indicators, this is absolutely NOT fool-proof…that would be far too easy! This should be used as another resource to help achieve success.

There is clear evidence that a sharp fall of the GLR precedes a sharp fall in the gold price by a day or two on numerous occasions and so this can be used to help make trading decisions – if you see this pattern emerging you have to question whether it is wise to take a long position.

The GLR is dynamic and affected by many different factors as it is a derivative of LIBOR and GOFO – it is always changing and therefore basing all trading decisions on whether it is rising or falling would be unwise.

From our analysis there is no direct correlation between the GLR and the price of gold per-se – but when a sharp fall of the GLR is sustained over 2 or 3 days it looks like a good time to go short!

Get more free articles like this helping you learn how to trade online.

You can get a 30-day historical view of the Gold Lease Rate at www.kitco.com and longer-term charts are available at www.sharelynx.com

There is clear evidence that a sharp fall of the GLR precedes a sharp fall in the gold price by a day or two on numerous occasions and so this can be used to help make trading decisions – if you see this pattern emerging you have to question whether it is wise to take a long position.

The GLR is dynamic and affected by many different factors as it is a derivative of LIBOR and GOFO – it is always changing and therefore basing all trading decisions on whether it is rising or falling would be unwise.

From our analysis there is no direct correlation between the GLR and the price of gold per-se – but when a sharp fall of the GLR is sustained over 2 or 3 days it looks like a good time to go short!

Get more free articles like this helping you learn how to trade online.

You can get a 30-day historical view of the Gold Lease Rate at www.kitco.com and longer-term charts are available at www.sharelynx.com